The Venn diagram overlap of people obsessively interested in both exchange traded funds and the risk parity investment strategy isn’t huge, but it includes at least one of the people at FT Alphaville Towers.

So here are some more, hopefully semi-coherent, thoughts on the news that State Street Global Advisors is partnering with Bridgewater to launch an ETF powered by the hedge fund group’s “All Weather” risk parity strategy.

Admittedly this content won’t be for everyone, but we’re told that niches are the future of journalism, so:

This is a weird time to be launching a risk parity product

State Street has been on an alternative investment product launching blitz lately, but it has mostly hit obvious red-hot areas, like private credit and crypto. Risk parity, on the other hand, is pretty untrendy these days.

Risk parity was first invented by Bridgewater’s Ray Dalio as a “forever” portfolio that was supposed to be more rigorous and truly balanced than traditional strategies like a 60-40 equities-bond fund.

In a 60-40 fund, equities in practice contribute the vast majority of the risk and rewards, because stocks are much more volatile than bonds. So Bridgewater’s All Weather fund — launched in 1996 — measures the mathematical volatility of each asset class and uses leverage to ensure that each contributes equally (vol-wise) to a diversified, passive portfolio.

The idea is that this more rigorously-balanced portfolio should do well in most market regimes. In practice, it means a slightly smaller equity allocation, more money in commodities and leveraging up the bond exposure significantly. As Bridgewater’s own All Weather genesis story explains it:

It did phenomenally well through both the boom and the bust of the 2000s — delivering both strong and relatively steady returns — thanks to the juiced-up fixed income component. All Weather therefore birthed a host of copycats that became collectively known as risk parity funds (because they seek to equal-weight the risk contribution of each component).

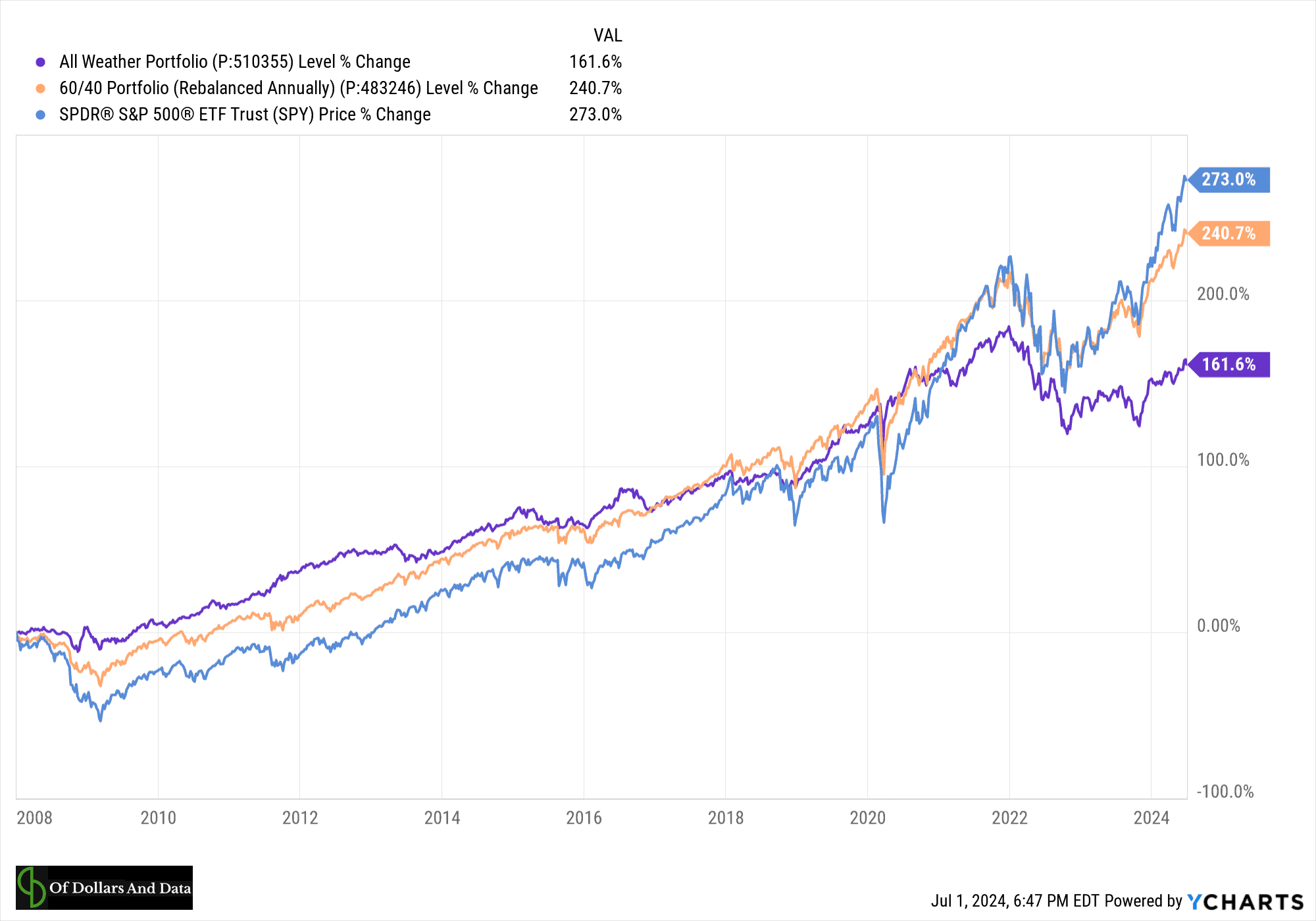

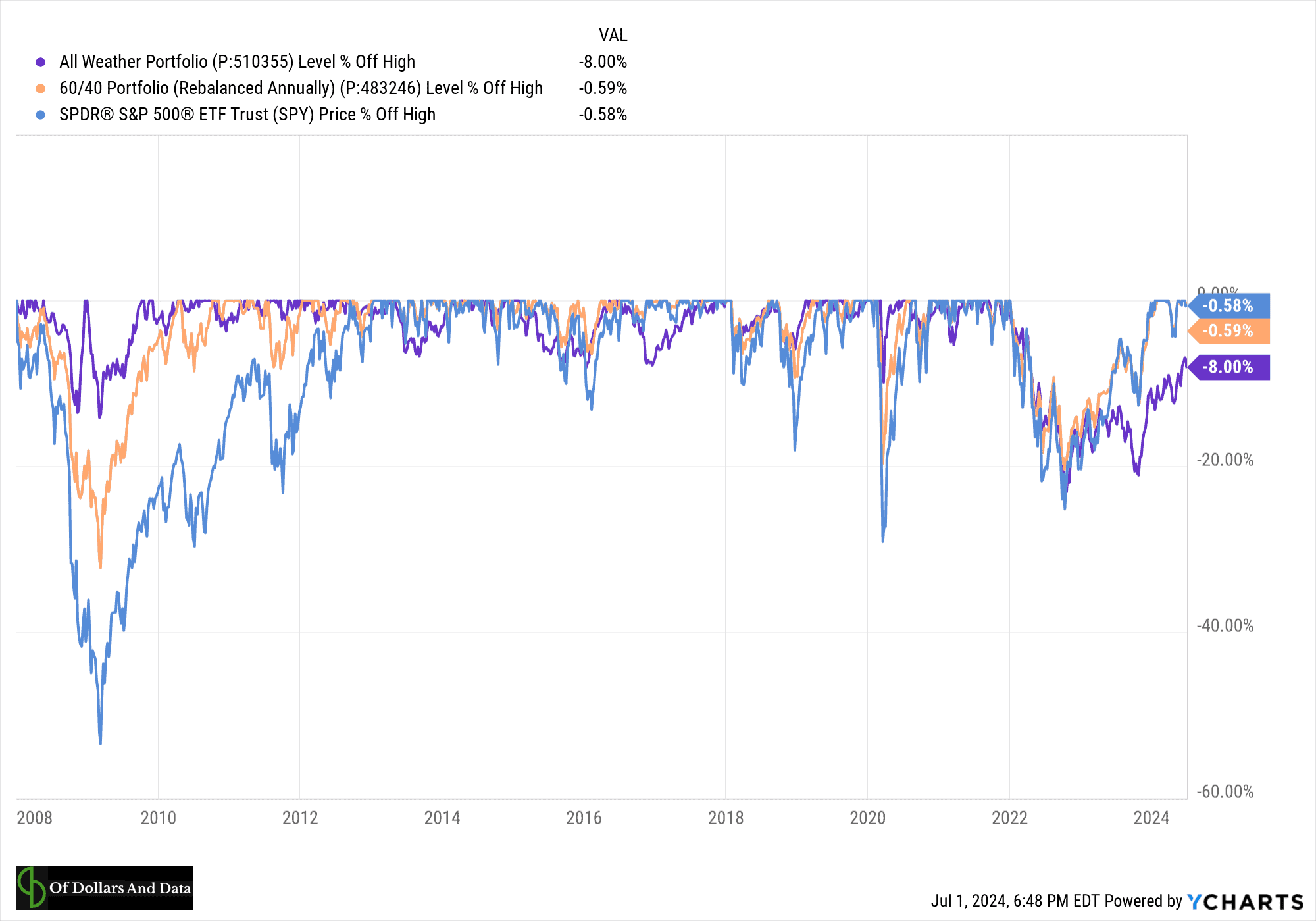

However, the bloom started to fade in the 2010s, and lately it has done markedly worse than classic 60-40 funds. Here are some great charts from Nick Maggiulli that show the recent deterioration:

(Sorry for visibility issues. Zoomable version of the first chart here and the second chart here.)

There’s no great secret to why All Weather specifically and risk parity in general have sucked a bit lately.

Leveraged fixed-income investing did well in the decades where interest rates generally trended down, but lately it has been exceptionally painful. The lower equity allocation also drags on performance relative to a 60-40 fund when stock markets are on a tear, as they have been recently.

The result has been billions of dollars slowly seeping out of risk parity funds in recent years, as investors lost faith in the strategy as a truly “all weather” strategy. As Fortune reported earlier this year.

“It’s been disappointing for a long time,” said Eileen Neill, managing director at Verus Investments, an adviser to New Mexico’s roughly $17 billion public employee pension, which axed its risk-parity allocation in December. “The only time risk parity was really successful was at the time of the Great Financial Crisis and that was really its heyday.”

Just a few weeks ago robo adviser Wealthfront announced it was shuttering its own risk parity fund. In Denmark, risk parity even became a political scandal after its largest pension plan ATP suffered a bout of terrible performance thanks to its adherence to the strategy.

In other words, this is a pretty contrarian time to be launching any risk parity product, let alone one aimed at retail investors.

An All Weather ETF still makes a lot of sense

The ETF structure has long since transcended its roots as a vehicle for passive, plain-vanilla US stock market exposure. Nowadays you can throw pretty much any crap into the ETF wrapper, and increasingly people are doing just that.

However, the passive, diversified, forever strategy that risk parity (in its idealised form) represents is perfect for ETFisation. There are no big technical or regulatory implementation problems. Daily transparency on its holdings will make it easy for market-makers to handle.

For State Street, this could be a big win. Although it pioneered ETFs and still manages the industry’s single biggest fund (for now) it has fallen behind rivals BlackRock and Vanguard on the big standard ETFs, while smaller and nimbler rivals have done better in more niche funds.

It is now clearly betting that alternatives will get it back in the game, and associating with Bridgewater — which is, despite some reputational blemishes, still the world’s biggest hedge fund group — is a big fillip, especially after also getting in bed with Apollo.

But this is also a potentially big deal for Bridgewater, which is still struggling to find its feet after a loooooooooooooooooooooooong and messy succession from Ray Dalio.

Its overall assets under management have now fallen to about $100bn, from a peak of nearly $170bn. Bottling up one of its best-known strategies and partnering with a traditional asset management giant like State Street could prove a winner that helps turns its fortunes around. For Bridgewater this opens up the $45tn US wealth management industry , and many financial advisers are likely to be intrigued.

After all, for all the recent woes suffered by risk parity strategies, the basics of the approach still make sense. And as we wrote earlier this week, Bridgewater’s All Weather fund is the “original Coke” of risk parity. Thanks to Ray Dalio’s huge profile there is a lot of mainstream knowledge of the firm and the risk parity approach, so this ETF will probably be a blockbuster launch.

But the details matter. A lot

The prospectus filed by State Street is missing a lot of crucial information, such as what the fees will be. That’s obviously a biggie. What might make sense at 50 basis points a year could be a no-brainer at 10 bps, or idiotic at 200 bps

Most of all, the filing is vague on the ETF’s exact strategy. State Street Global Advisors will be the investment manager, while Bridgewater will be the sub-adviser. Here’s how the prospectus describes how they’ll work together:

Bridgewater provides a daily model portfolio to SSGA FM based on Bridgewater’s proprietary All Weather asset allocation approach. The model portfolio is specific to the Fund. Based on Bridgewater’s investment recommendations, SSGA FM purchases and sells securities and/or instruments for the Fund. SSGA FM seeks to implement Bridgewater’s investment recommendations, but may change the Fund’s investment allocation at any time.

Look, we have questions. Lots of them.

Even if we accept that the language around State Street merely receiving investment “recommendations” from Bridgewater and being able to ignore them “at any time” as legal caveats, it’s not clear just how similar this model portfolio will be to Bridgewater’s actual All Weather strategy.

All we know is that Bridgewater’s co-CIO Karen Karniol-Tambour and head of balanced asset strategies Christopher Ward are responsible for constructing the model portfolio, while the actual fund managers at SSGA are James Kramer and Michael Martel, assisted by two less senior portfolio managers.

Bridgewater offers institutional investors different flavours of All Weather according to their tolerance of volatility. Risk-averse investors might prefer the steadier 8 per cent volatility AW portfolio, while others want 14 per cent. The prospectus says that the State Street/Bridgewater All Weather ETF will have a volatility target of about 10-12 per cent — so close to the standard All Weather approach — but little beyond that.

This opens up a phenomenally tricky balancing act. If Bridgewater sells something extremely similar to the canonical All Weather strategy in a presumably cheap ETF wrapper then it could cannibalise one of its core products (even though it seems you can invest for free in All Weather if you have an equal investment in the pricier Pure Alpha hedge fund).

On the other hand, if it ends up selling a shoddy version of the real deal to retail investors there could at the very least be reputational fallout. Just look at the years of heat Wealthfront took from its own stab at replicating All Weather, before the announcement earlier this month that it was killing its version.

Radical transparency?

As we mentioned earlier, the prospectus indicates that the All Weather ETF will each day publicly disseminate all of its holdings and the baskets of securities it will accept to create new shares. That will make it easy for trading firms to make markets in the ETF, but it raises a lot of questions.

Despite espousing a philosophy of “radical transparency”, the reality is that Bridgewater is phenomenally secretive. Even internally, knowledge of what actually happens inside its “investment engine” is extremely closely held. And now Bridgewater is supposedly going to disclose daily at least roughly what its All Weather models are spitting out?

Yes, this isn’t the “Pure Alpha” hedge fund’s strategies, but the details of All Weather’s allocations are also treated akin to the nuclear codes. I once sat through several hours of Bridgewater tutorials on the fund and still didn’t get much more than the box we showed above.

In other words, the disclosure of an All Weather model portfolio will at best be an awkward cultural issue. But it will no doubt be pored over by rivals keen to model the flows and see what can be exploited. And again, if the model portfolio handed to State Street is dramatically different from what Bridgewater actually does internally, the optics of marketing the fund with the “All Weather” brand all over the investor documents could be . . . suboptimal.

Bridgewater declined to comment, citing SEC rules prohibiting discussions of investment products before they have been approved.

{kind=link}

{kind=link}