Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

It’s Monday morning so let’s get this done.

Grating American roast voice:

Wow, FT Alphaville writes about Bank of England QT so much. Forget Unhedged, they should launch a newsletter called Unreserved!

. . .

It’s been a long six days since we last wrote about the BoE’s efforts to whittle down the massive pile of gilts brought into the Asset Purchase Facility by quantitative easing. So let’s go again. If you haven’t read that piece, or have no idea what we’re talking about, go read that piece first.

As we wrote in that piece, QT is currently affecting the UK economy in a number of unclear ways. And, as that piece emphasised, Britain’s fiscal framework means one of the most pertinent questions around QT is how the Office for Budget Responsibility chooses to forecast it.

At present, the OBR expects active sales of £48bn every year until the end of its forecast (2029/30), topping up variable levels of passive reduction via gilts maturing.

And, as we wrote in March, that figure is nonsense: it’s little more than a guess, born out of partial data, crude extrapolation and analytical dereliction.

But let’s leave the OBR’s forecasts for now, and rejoin the real world.

For the first two years of QT including active bond sales, the Monetary Policy Committee has topped up the passive roll-off of maturing bonds with active sales in order to target a total annual reduction of £100bn.

As a result, the baseline assumption everyone seems to be working against is that the annual envelope from this September will once again be £100bn, implying £51.9bn of active sales.

However, we noted that we’re seeing a range of forecasts for what the QT envelope for 2025/26 will be, and on Friday Bank of America joined the fun with an interesting bid of just £60bn, implying only £10.9bn of active sales.

BofA’s Sonali Punhani and team write:

We are sceptical whether QT is really operating in the background, not least in light of recent long-end Gilt price action. BoE research is also raising concerns that QT could be tightening monetary conditions more than expected, having a restrictive impact on the economy.

At a time when the BoE is trying to ease monetary conditions by cutting rates, QT could be diluting the passthrough of cuts by tightening monetary conditions at the long end. The transition from Quantitative Easing (QE) to QT has magnified the large upward adjustment in effective supply from the Debt Management Office (DMO) and BoE combined. In our view, the QT pace- and the fact that QT has had an active component that is unique to the UK- has been a contributing factor to the underperformance of long-dated Gilts versus overseas peers.

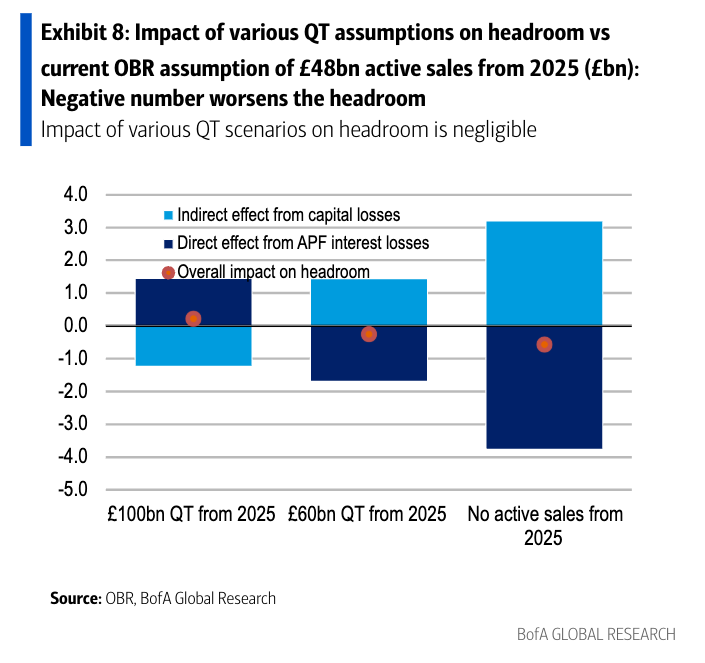

Helpfully, they’ve done some scenario modelling:

— Current £100bn total runoff continues- This would imply a £600bn reduction in APF in QT years 2024-29, £92.2bn more than the OBR assumption. This is likely to reduce APF interest losses by £1.4bn. But this would also mean active sales are £92.2bn higher by 2029-30 relative to the OBR assumption. Assuming these bonds are sold at 2/3rd their purchase price, this would mean losses crystallized could raise overall debt by £31bn, which could add £1.2bn to debt interest costs. Overall, we get a £0.2bn improvement to the headroom (Exhibit 8 and Exhibit 9).

— Our base case of total £60bn runoff from QT year 2025– This would imply a £400bn reduction in APF in QT years 2024-29, £107.8bn less than the OBR assumption. This is likely to increase APF interest losses by £1.7bn. But this would also mean that active sales are £107.8bn lower by 2029-30. This would mean losses crystallized are lower, which could lower debt by £36bn and debt interest costs by £1.4bn. Overall we get a £0.3bn worsening of the headroom.

— No active sales from QT 2025- This would imply a £267.8bn reduction in APF in QT years 2024-29, £240bn less than the OBR assumption. This is likely to increase APF interest losses by £3.8bn. But this would also mean that active sales are £240bn lower by 2029-30. This would mean lower losses crystallized which could lower debt by £80bn and debt interest cost by £3.2bn. Overall we get a £0.6bn worsening of the headroom.

[Zoom]

None of these are big numbers. And, as BofA notes:

This negligible hit to the headroom could be more than offset if slowing the QT pace ends up lowering long end gilt yields.

At the risk of banging a drum until it ruptures, the fundamental impact of active QT is an unnecessary upwards pressure on gilt yields that — however the accounting quirks and fiscal rules end up working in the short-term — presents a large long-term cost to the UK.

Now, the MPC obviously isn’t really obliged to care about this, beyond some value-for-money concerns. A Bank Overground piece published today confirms that the institutional view from Threadneedle Street is that QT is operating fine, thank you. Vicky Saporta’s speech about the BoE’s balance sheet, set to drop next week, may offer more interesting insights into how the central bank sees this process playing out in the markets.

Still, things are now looking pretty open for the next QT decision, which will land at the end of summer.

There’s even a chance — as TD Securities’ Pooja Kumra notes — that the BoE shows its hand later this month. As she wrote in a note published yesterday:

The BoE is set to release the next quarter QT schedule on June 20. We would expect that it should comprise 1 short/1 medium/1 long auction. To us, if the BoE again replaces the long auction with a short/medium auction – it would be a clear signal of active sales nearing their endpoint.

What that would imply for the MPC’s role in determining how QT should operate is an open question.

There is, we suppose, the possibility that enough of its members also wear financial stability/BoE operations hats (more on that here) that its generally-dominant core of internals can basically dictate how the vote goes, and that includes potentially front-running it. That could prompt further questions about how truly independent the MPC is.

The practicalities, in either case, are a bit weird. Voting for Bank Rate is easy from a practical perspective: everyone names a number along a quarter-point spectrum, and the most popular number wins.

Active QT is much more granular. With unanimous votes in the first few years, things were simple. But it looks like that could change: in the past week we’ve seen sell-side predictions of active envelopes at £50.9bn, £30.9bn, £10.9bn and £0bn, and Catherine Mann is starting to make noises.

If the MPC does end up divided over this, it may present a practical challenge. Will everyone just shout random numbers until there’s a consensus? Maybe having a bloc set the terms is helpful.

Further reading:

— Britain’s quantitative tightening will hurt us for a long, long time

— The Bank of England’s bond sales might finally become a hot topic. Does the OBR care?

{kind=link}