Todd H Baker is the managing principal at Broadmoor Consulting and senior fellow at Richman Center for Business, Law and Public Policy at Columbia Business School and Columbia Law School.

Circle Internet is the issuer of USDC, one of the largest fiat-backed stablecoins in the world, with around $43bn in circulation.

The company filed an S-1 last month for an underwritten IPO but despite the backing of underwriters JPMorgan and Citigroup and an indicated $5bn valuation, it’s been hard going. This is the second time Circle has tried to go public, it having pursued a Spac deal at a $9nn valuation in 2021 that never made it to the finish line.

Perhaps the tariff-induced market freeze explains why Ripple Labs reportedly made an offer to buy Circle for $4-$5bn, which management rejected as too low. Unsubstantiated (and implausible) rumours then went around social media that Ripple had raised its offer to $10bn or even $20bn. What is going on here?

If we look just at vibes, it seems like a high-tech-darling price for Circle might be reasonable. What is hotter right and more on-trend right now than fiat-based stablecoins? This is the year of crypto in the US, and stablecoins are the poster child for the integration of crypto tools into the financial system. Maga loves stablecoins! Kristen Gillibrand loves stablecoins!

News Flash: Circle isn’t really a tech play at all. Financially, Circle is a highly levered, uninsured narrow bank with nearly all of its revenue coming from a big bucket of short-term cash investments. It makes money when rates are higher, up to a point, and makes less or loses money when rates are low.

That makes Circle a market play on — or a plaything of — volatile short-term interest rates, with another big dollop of revenue volatility tied to estimates of future crypto trading volume, beliefs about blockchain inevitability and who will be the ultimate winners if stablecoins go mainstream.

Narrow banks take in money from customers as deposits, invest that money directly in Fed Funds with zero credit risk and pay interest at a slightly lower rate to their depositors. They don’t do maturity, credit transformation or much else, so their operating costs are low.

The bonus with Circle is that you can use the tokens that represent your deposit to pay for things, with a blockchain record that says you have transferred some fiat money on deposit with Circle to someone else. It’s not unlike regular money transfers, if all parties were depositors at the same bank and the funds transfer was internal and notional.

The Cato Institute libertarians love the idea of narrow banks, because they would replace the dreaded deposit insurance system with a free-market solution and allow consumers to hold safe deposits while freeing lending from the deadly shackles of regulation and gifting lenders with the blessings of market funding. Up to now the US government wasn’t so keen on the idea. Regulators have been unwilling to support a “bank” that doesn’t engage in lending.

Like a narrow bank, 98 per cent of Circle’s revenue is interest on the securities holdings which back its stablecoins.

But there are a few differences between Circle and the Platonic ideal of a narrow bank. Unlike a true narrow bank, its liabilities (coin-holder “deposits”) are non-interest-bearing (because otherwise fiat stablecoins are securities under US law, or at least they are until the last person left at the SEC forgets the rules.) That means that Circle is unable to use deposit costs (which at a narrow bank might equal 40-70 per cent of interest revenue) to manage towards a stable (or at least predictable) net interest margin like a bank but instead is fully exposed to the impact that changes in market interest rates have on revenue.

That’s good when the rate gods are smiling and bad when they frown because it amplifies the impact of rate movements.

Yields on Circle’s securities portfolio over the past three years have varied between 0.14 per cent and 5.17 per cent, during which time Circle moved from $38mn in operating losses in 2022 to operating profits in of $269mn in 2023 and $167mn in 2024.

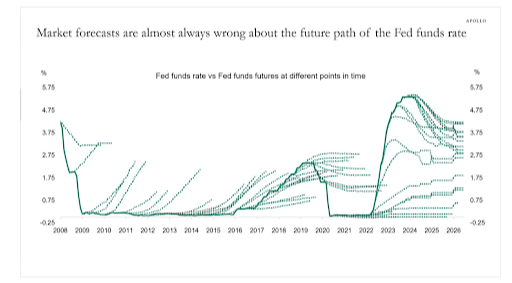

This then brings us to the unanswerable question at the heart of Circle’s business: Does anyone know where short-term interest rates will be in the future? Will Trumpenomics and tariffs cause inflation and higher rates? Or trigger a recession and lower rates? Or cause stagflation where rates will do, what exactly? Nobody knows. Not even Jay Powell.

You could bet on projections like this . . .

But since market forecasts are almost always wrong, your chances of getting it right are limited. It’s a random walk. Good luck projecting revenue for this baby.

Circle admits how little it controls its destiny. As Circle’s founder Jeremy Allaire says in the S-1:

We have faced challenges. For example, in 2023, USDC went through an extended period of circulation decline related to a number of factors, including an increase in us short-term interest rates, a decline in digital asset prices, and an associated decline in leverage in the digital asset trading ecosystem, as well as the impact of a temporary price dislocation in the secondary markets in March 2023 resulting from the collapse of certain us regional banks that caused some market share to move to a competitor. We will no doubt continue to face challenges in the future.

There’s big talk but little real action so far turning stablecoins into the new international payments rails. The US, UK and European governments, for some hard-to-fathom reasons, are currently trying to import stablecoins into the real payments system, despite a lack of demand to do so, no real cost justification and huge interoperability and fraud/cyber security problems.

Many in the US (including Allaire, an enthusiastic proponent) currently think a stablecoin law will be in place by the end of 2025, with the hope that this will trigger a blizzard of new stablecoin issuers and mass adoption of the technology. It’s a tight deadline. Senate Democrats have threatened to filibuster stablecoin legislation over what they see as failings around anti-money laundering, foreign issuers, national security, accountability, and “preserving the safety and soundness of our financial system”.

But let’s say Allaire is right and stablecoins are the future for at least some of the payments system. What does this mean for a standalone Circle?

Does Circle have any special sauce that can’t be reproduced by new competitors, particularly those with big names in finance? History suggests not. At bottom, Circle’s business is extremely simple and easy to replicate: take money in, invest in T-bills, send money out, pay marketing partners (instead of depositors) and keep track of it all on a blockchain.

Circle has some scale advantages. Even if USDC issuance and its balance sheet increase materially over time, its fixed costs are likely to continue to be relatively stable. But scale only matters if scaling is costly. It’s relatively trivial to build a stablecoin now that the pattern has been set. If real world adoption picks up in a government regulated market, who will be likely to benefit? My guess is the big banks, big crypto trading outfits or big tech companies that dominate real world applications. Circle will get the leftovers.

And due to its utility-like place in the crypto universe, Circle receives no material revenue associated with USDC secondary trade. That’s because, although it issues USDC and holds the offsetting assets, it’s not generating revenue from trading or staking transactions involving the stablecoins in either the cryptoverse or the real world. All that counts are the cash balances. Others in the cryptosphere are making all the money. Circle is just the holder of the swag.

Moreover, Circle actually pays Coinbase and others in the cryptoverse most (over 60 per cent) of its interest earnings as part of revenue revenue-sharing arrangement associated with the distribution of USDC by brokerages and various other crypto intermediaries. That alone suggests there’s nothing special about USDC and emphasises how little control the company has over its own destiny.

Here’s the nugget about that in Circle’s S-1 disclosure:

As a result, distribution costs are impacted by the actions and policies of Coinbase and their effects on the amount of USDC in circulation held on Coinbase’s platform, which we do not control or oversee.

Want to figure out how distribution costs may change in the future? The relevant note is on page 101:

All in all, a pretty pedestrian business for a crypto world used to high risk and high reward.

In the most convincing framing, Circle as a standalone entity is worth what a narrow bank with very low credit risk, very high-interest rate risk, a 60 per cent revenue haircut, no interest expense and a challenging competitive environment for growth would be worth. That probably means something close to book value (which was a little less than $2bn pre-IPO).

So, what might be Ripple’s motivation for boring crypto utility?

Ripple itself is a big bet on the ultimate triumph of blockchain finance over traditional systems in the payments area. So far, its ambitions in this area have depended on XRP, its internal, centrally managed, non-fiat crypto coin. XRP is meant to facilitate larger, institutional financial transactions as a bridge currency. Ripple supports RippleNet, a fast, inexpensive global payments network, which doesn’t require its institutional users, such as banks and other money transfer companies, to “pre-fund” accounts with cash to make payments.

The XRP Ledger enables users to conduct transactions in any currency they choose — whether fiat, digital assets, or other forms of value — alongside XRP. This flexibility is especially valuable for cross-border payments, as it allows users to send and receive funds in their local currencies without needing to manually convert between them.

Although it has been around for 13 years, Ripple has barely made a dent in the real-world payments. XRP payments volume runs around $1bn a day, most of it from speculative crypto coin activity, including sales by its founders.

XRP itself has become a volatile, speculative cryptocoin and that risk makes Ripple a less attractive candidate for inclusion in the traditional financial system than a fiat-backed stablecoin like, for example, Circle’s USDC.

The industrial logic for Ripple buying Circle seems clear if you are a crypto maximalist. Ripple today generates revenue through several channels: the sale of XRP, transaction fees, returns on investments, and interest on loans, although how much it earns from sources other than token sales is anyone’s guess, as Ripple remains private.

Ownership of Circle’s USDC would provide Ripple with a valuable alternative set of payment rails to expand its real-world business, as well as additional revenue from USDC’s existing reserve assets. Ripple has experience connecting the cryptoverse with the real financial system and it has the brand presence needed to keep USDC relevant in the free-for all competitive environment that is coming with government-sanctioned stablecoins. It might even be able to negotiate lower “distribution costs” from crypto players over time.

One must assume that any Ripple offer would be all, or mostly, in the form of unlisted Ripple Labs stock, so Circle shareholders would be exchanging one relatively modest long-term bet on real-world crypto adoption for a larger and much riskier bet. Believers will see that as a good trade, while those Circle investors looking for liquidity shouldn’t hold their breath.

{kind=link}

{kind=link}